It’s not a secret that Microsoft’s future depends on Azure not only being successful, but dominant. With Google Workspace dethroning Office 365 in the cloud productivity markets, Windows needing a complete re-write since a decade ago and their consequent monopoly on exploits and ransomware attacks in the PC and Server markets, much is riding on Azure’s ability to dominate the cloud infrastructure space as Microsoft has done with the OS, productivity, and server spaces before.

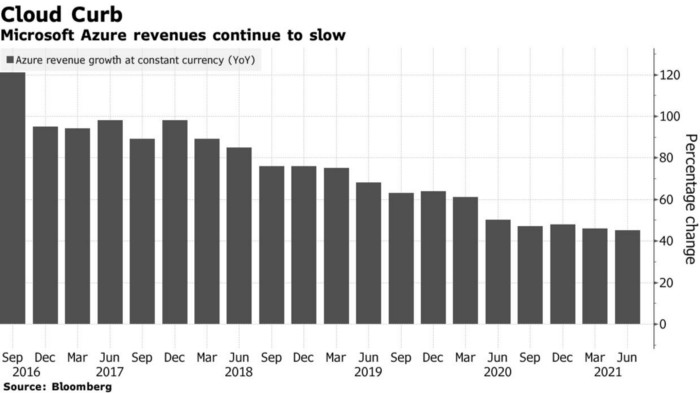

One consequence of Microsoft’s dependence on Azure is that Microsoft can post its best quarter ever and investors will get spooked if Azure’s revenue growth slips in the slightest. It also doesn’t help when their CFO Amy Hood admitted that Azure slowing revenue growth still performed better than she anticipated.

“Forty-five percent was both better than we expected and driven by consumption growth, which is very good,” Hood said in an interview. “Demand is healthy. The overall execution was better than I expected.” -Amy Hood

Unlike before though, Microsoft isn’t starting at the top as it did in the OS, Productivity, and Server spaces. Instead, Microsoft was 2 years late to the market and has to compete with the likes of AWS instead and claw market-share away from them. And this is bad news for Microsoft as competing with other tech monopolies in established markets is not something that they’re especially good at; they aren’t the same company that mothballed IBM all those years ago.

The success of Microsoft’s business model relies mostly on them being among the first movers of infant markets, becoming the industry standard, and entrenching its products throughout said industry; lock-in if you will. In turn, their products no longer need to compete on quality, cease to evolve, and stagnate no differently than the human race as they have no ecological competition. Apparently, the law of natural selection even applies to markets.

In doing this, Microsoft’s frustrating, insecure, and unstable architecture renders users change and technology averse, traumatized if you will, and consequently vying to keep everything the same. Further, they can artificially inflate the switching costs of moving to their competition, derail migration efforts to their competition even if it’s better technology, and maintain dominance. Put simply, Microsoft’s products and services create a moat of sorts that keeps users in and competition out while allowing them to compete with themselves. Mitigating their defenses is much easier said than done.

Being a first-mover that optimizes their solutions for lock-in is a double whammy for Microsoft and no one seems to care; hence why they do it. This happens to be why Windows, Active Directory, Server, and Exchange are still in play today despite being legacy, expensive, complex, frustrating, and unstable for users and admins alike. It’s simply too ingrained and users/admins are rendered apathetic to change.

While Microsoft can’t exactly take credit for this brilliant aspect of their business model, they can absolutely laugh all the way to the bank at anyone who is criticizing them about their quality woes without realizing that they don’t even have to compete on quality; at least until Azure became their last hope.

One immediate problem with their tactics though is that they don’t bode well in markets that are already well-established nor is it easy to re-structure a company to engineer for quality when it’s structured to maximize lock-in. Although absolute genius goes into engineering products for lock-in, especially when realizing that all of their engineers are trying to do their best/ethical job, this heroin-esque approach to engineering is systemic and cannot be turned off like a light switch; quite the contrary. Any manager at Microsoft can and will affirm that Microsoft is a big ship to steer and such a restructuring could take years to fully implement.

As such and much like their founder Bill Gates, Microsoft isn’t equipped for fair competition, hence why they lose their ass in markets they’re late to, nor are they known for being a good sport at that. And as they have shown repeatedly with cloud, mobile, social, gaming, and laptop markets, Microsoft is consistently a fish out of water when entering well-established markets because they are not optimized to compete on quality which is the only card that a new entrant has to play against the status quo; exhibit Zoom and Slack. All of which stacks the deck further against Microsoft’s ambitions with Azure.

To highlight this and although Microsoft is doing great things in the cloud space with Office 365, they were late to the market, ironically among the last to host their own services, and are in second place while losing further ground to Google Workspace. The same is true of Azure in that it was 2 years behind AWS to the cloud infrastructure market.

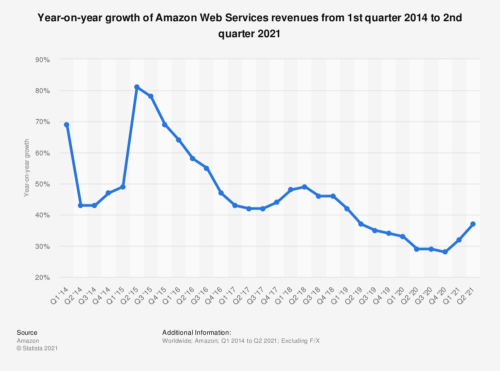

And although Microsoft and analysts claim Azure to be second in the cloud infrastructure space from a revenue perspective, Microsoft has yet to corroborate this with data and is refusing to post individual performance metrics of Azure after a decade of production. Based on what little we’ve seen though, AWS revenue is growing while Azure revenue growth is shrinking which is the opposite of what Azure needs to do. Meanwhile, AWS revenue grew 9% in the last year.

No matter where you look, you can find Microsoft consistently omitting all key performance indicators (KPIs) worthy of mention concerning Azure financials or usage; MAU, P&L, CPA, ARPA, RPE, etc; nada. Meanwhile, you’ll find a whole host of ambiguous metrics such as vague growth rates, total user counts instead of monthly use statistics, and containers like the Intelligent Cloud averaging various offerings together. All of which takes significantly more effort than simply reporting individual performance and is frankly hard to keep under wraps for 12 years. Meanwhile, AWS has no problem reporting on AWS’s performance; they have nothing to hide.

Oddly enough though and while it’s even their policy to never report on KPIs, they definitely track them and occasionally post them but only if they exude a dominant market presence. In doing this though, Microsoft has a tell so to speak. Put simply, when products are doing fantastically, Microsoft will break protocol from time to time and report KPIs. But when products are doing horribly, Microsoft seems to hide behind their bogus policy so as to keep KPIs under lock and key while sugar-coating poor performance with ambiguities instead.

In doing this though, this being not reporting common usage and financial metrics while further hiding individual performance in the Intelligent Cloud, Microsoft has made it impossible for analysts to evaluate where Microsoft stands in the fold compared to AWS or Google Cloud. Ironically, the assessments declaring Azure to be in second place among cloud providers are speculative at best.

“Muddy waters make it easy to catch fish.” — Chinese Proverb

With all of this in mind, it’s easy to see why Microsoft needs investors to believe that Azure’s position is strong and why Microsoft is working so hard to keep Azure’s performance under wraps; that dog don’t hunt. Although I can only speculate, it seems as if the KPIs surrounding Azure do not exhibit dominance or a route to dominance that Microsoft needs to project in order for share prices to keep rising while its stagnant revenue growth serves as further evidence of this.

If said KPIs did exhibit Azure’s dominance or even a route to dominance, then Microsoft would have no reason to be shy and release them in the face of increasing scrutiny of their persistent refusal to report on these metrics. And their refusal to post these metrics while muddying the waters with pointless statistics/rates and odd financial containers instead isn’t exactly a good omen so far as the health of Azure is concerned; if not symptomatic of the contrary. Put simply, if Azure truly had a big ol’ dong then Microsoft would have thrown it on the table by now rather than hiding it behind excuses and obscure metrics for over a decade.

To be fair though, Microsoft could indeed be shy about Azure’s performance for the past 12 years. Azure could be doing great for all I know. What I do know is that omission is the most common form of lying with statistics, followed by obfuscating matters with bogus metrics, and Microsoft doesn’t have an incentive to resort to these squid and ink tactics if Azure is in great shape. All stars go through an inflationary phase before they go supernova.

You’re welcome to believe otherwise though. You’re welcome to believe that the 71.355 billion Microsoft spent on stock buybacks since March of 2018 were made to benefit the shareholders too; but that’s for another day. ⬆

Surely if we had properly-functioning media, then someone would investigate this rather than rely on official statements from Microsoft and WARN notices

In the domain of Free software, there are very few sites out there that offer exclusive coverage on community affairs and there are many gagging/censorship attempts